Canadian Thanksgiving already? Where did the time go! I feel like it was just 3 months ago that I was on an airplane going on vacation and writing my forecasting obituary. Q2 was not solid. And I have this gut feeling that Q3 isn’t going to be much better, notwithstanding the scintillating run-up in oil prices that we saw in September (only to give back… in the last few days).

But I have to do my review. Even if it’s a long weekend and even if this turkey, to belabour the metaphor just a bit more, won’t fly. It’s been a hell of a run with the Fearless Forecast and I refuse to give up but markets are weird and fickle things. Where on the one hand a value based approach seems like the right approach, what are you supposed to with a market that rewards a car company’s share price (Tesla) when it announces declining sales and massive increases in inventory even as it slashes prices.

Some things will never make sense to me. Like 20 times revenue as a valuation metric. Or companies with historically low levels of debt and gushing cash flow being valued as if they are Canadian oil and gas companies. Oh wait – that’s exactly what they are!

So as I like to say, crap.

At any rate, it’s time to pay the piper, stand up and be seen, self-assess and self-reflect. Despite the trepidation, there is no need to be ashamed of these forecasts. I do it every year. Sometimes I’m close, sometimes I’m way off.

I mean it’s not like any of you take these predictions as any kind of advice or make economic, financial and/or investment decisions based off my POOMA (pulled out of my ass) prognostications – right? Please tell me that I at least have that part right?

Hmm – well that problematic thought aside (like really people, so much of this is tongue in cheek – be smart!), I do put a little effort into it, so I appreciate you sticking around to see how I did, even if it is only to watch me squirm.

Whatevs – here we go.

As regular readers know, I changed up my format this year. Rather than a long blathering narrative, I instead made 30 (less long and blathering) predictions that I am going to review and give a progress report on. This way I can get an actual numerical/percent grade at the end that allow for objective assessment rather than my traditional self-serving and 100% subjective approach.

So below – the forecast reprinted with a self-assessment after each of the 30 bold predictions. I hope this is easier to follow. It’s a long read, if you want it to go faster – anything in bold is a prediction, anything italic is the self-assessment.

Broad Themes

In developing the Forecast, I centred my thoughts as much as possible around the following three themes which I believed, at the time, would be the most relevant over the course of the year.

- The rising I’s have it. Inflation and interest rates

- Energy Security vs Energy Transition

- To Recess or Not, that is the question

Each of these will in some way inform and influence all that follows

Politics and Stuff

- Sorry folks but I am guessing there will be an important election in Canada this year and, no, it won’t only be in Alberta. The Trudeau government, as long in the tooth and economically inept as it is, and the Liberal Party of Canada have been acting like a majority for a while but are getting as tired of Jagmeet Singh as the rest of us are. They want their very own majority. And they smell blood in the water. Pierre Poilievre, as talented a woodworker as he is, is so far not demonstrating any traction with voters located anywhere east of the Saskatchewan border or voters who don’t have well, you know, too much testosterone. I am figuring a fall election that will allow Trudeau to either campaign against the evil Danielle Smith and her environment and constitution-wrecking ways or to hold up a Notley NDP victory in Alberta as proof that progressivism is ascendant across the land. Oh, and the Liberals will win a majority, despite Trudeau, who will finally resign in 2024.

Well, this one is easy. There will be no fall election. But the scandal ridden and tired Liberal party needs to go. Trudeau is mailing it in and his numbers are cratering, but Jagmeet seems incapable of tripping up the government by pulling out of the arrangement the NDP made. Maybe the whole pension story is true but in actuality I think the NDP is in worse shape than the LPC so it’s mutual misery arrangement. So, no election, just near constant electioneering – no one in government wants to face the electorate with all the headwinds of housing prices, inflation and affordability.

- Speaking of Alberta. We will have an election in May of 2023 and I can confidently predict a majority government for Rachel Notley and the NDP. I can confidently predict it, but I don’t believe it. I think the UCP and Danielle Smith will eke out a victory. Not because they earn it or represent a platform that people want, but because that is what the land sharks in the LPC want to campaign against in the fall so they will use the next few months to needle and provoke the UCP, Smith and Alberta to the point where we all get our backs up and want them to get the heck out of our lives. Why? Because. That’s why. Did you see the poll where Quebec was vastly more in favour of even tighter environmental policies than anywhere else in Canada? No? Well Trudeau did. There are a lot of seats up for grabs in Quebec and if Ontario is static, Quebec is the only place with enough seats to deliver a majority (sorry Maritimes).

Ironically, despite all of her various missteps in the past few months, this prediction came to pass. It was really close, the UCP eked out a small majority (by Alberta standards) thanks to rural Alberta and just enough seats in Calgary.

- South of the border, 2023 is shaping up to be … another annoying year of rabid partisanship, gridlocked government, Hunter Biden’s laptop, nutbar fringe republicans, far left dems threatening to wreck a good thing, will he or won’t he Trump threats and Sleepy Joe Biden delivering on his legislative agenda while his party questions his competency to sit another term and the GOP accuses him of doing nothing on all the issues they are obstructing. Dysfunction, thy name is Washington DC. OK, rant aside, the results of the US midterms have yielded a narrowly divided government that is going to be hard-pressed to deal with some of the big issues confronting the country. That said, I have confidence that former action super-hero, Heisman and Super-Bowl winning, inventor of the fax machine and Warren Buffett investment advisor George Santos, the newly elected congressman from New York will bring everyone together and solve whatever issues need to be solved. From a Canadian’s perspective, it would be a welcome change to see Trumpism finally go away – really just Trump – and have politics go back to the normal “left-right” divide but it feels like we will need one more punishing election cycle for the GOP to realize that ETTD (everything Trump touches dies) is not just about various failed business ventures. Aside from fear of MAGA, the Republican party lacks anyone who has the charisma and fire in the belly to truly offer an alternative to Trump so until such a beast emerges, this is the political reality. Ron de Santis seemed like he was an emerging force but the enthusiasm isn’t there. Don’t get me wrong, Trump is now down to a mere plurality of support, but change takes time. Similarly, no one on the Dem side has a chance of beating Trump aside from Grampa Joe Biden. The youth movement in American politics is one election cycle away barring criminal charges on either side, which seems increasingly unlikely.

Well, who would have thunk it. Trump actually got indicted – a whole bunch of times! Which of course only made him more popular. With his base. Don’t get me wrong, he’s still a virtual lock to win the nomination because of his base. The problem is that while the base loves him, no one else likes him. But my prediction stands – we need one more election cycle to wash out all the laundry on both sides and let the youth movement in.

- In the rest of the world, the name of the game is conflict and taking sides. The chief architect of all of this is of course Vlad “the Impaler” Putin and his ill-advised and criminal invasion of Ukraine (which I totally whiffed on last year). I do not foresee any significant de-escalation in this conflict as the bare-chested buffoon continues to call up 100s of thousands of new conscripts to be used as cannon-fodder for an increasingly well-supplied and battle-hardened Ukrainian army. There is no victory in this war. He has to know that. But the battle of attrition that it has settled into could easily go on for years. Meanwhile, the rogue’s gallery continues to misunderstand NATO’s steadfastness against Russia and aligns themselves with a losing proposition. This includes Iran and North Korea. China remains an enigma. They want Western money (you don’t get rich from trading with Russia) but need Russian energy and commodities. Plus, they hate Western democratic leadership and want free reign in Asia. India is only interested in India. My prediction is the war in Ukraine doesn’t end, Russia continues to self-destruct its economy and China begins looking for opportunities to realign West as outcomes become clear. Iran may explode into civil war as protests continue and the prospects for any kind of freedom concessions from the clerics seem non-existent. Netenyahu in Israel stirs the pot, so the Middle East is a bit of a powder keg. The much-feared Taiwan invasion is off for another year – domestically in China the anti-COVID protests were a clear signal to those in charge that they don’t have the iron fist they thought they had. Africa continues to be an afterthought to most of the “first world” except as a repository of minerals and in South America, the shift to the left continues.

Well, this one is a bit of a layup. Currently batting 0.950 with only China being an outlier with its half-hearted attempts to be seen as a global diplomatic peace-maker. We will see how that plays out as the Ukraine conflict approaches its second year anniversary.

- Will we have a recession? I don’t know. What do I look like? A forecaster? Yeah, yeah. Here’s what I think. There will be a recession. But the question you should be asking is if it is going to a real, textbook recession or is it going to be a recession of perception or a media recession. If the former, the odds are less than 90%. If the latter, I have news for you – we are already there. The objective reality is that runaway inflation, rising interest rates and the US dollar wrecking ball have already done their damage and are forcing the demand changes that central banks want to rein in inflation. But these policy instruments are blunt force trauma to the economy – the effects can be severe. Different economies will experience it differently. Whatever form the slowdown takes, it will be more severe outside the United States. Here in Canada, I feel it will be deeper and more drawn-out than in the United States mainly because our economy isn’t as resilient or dynamic as that of the United States and our over-dependence on elevated real estate prices rather than productive assets and attendant elevated levels of variable rate consumer debt is an Achilles heel. Could the effects be muted by commodities? Yes. Does the Federal government see that? I doubt it. Regardless of how long or deep a downturn might be, I am hard-pressed to see any recovery being much more than muted. Yes, the central banks now have policy room, but what is the catalyst for growth in the next several years? We have done tech, real estate, consumer goods, crypto, emerging markets, energy, renewables and social media. What’s left? Population growth, consumption and war.

I’m starting to think I was too pessimistic here, especially as it relates to Canada, but it’s still early and a lot can change. Economic numbers in Canada are holding up, but tenuously. And south of the border, while employment growth is slowing and the banking sector remains on shaky footing the economy refuses to tip over. It is truly a riddle wrapped in an enigma boxed up in a conundrum. Central bankers must be losing their minds. Ah, who am I kidding. They love this stuff.

- Driven by still high levels of energy insecurity and high prices, the energy sector is going to continue its gradual transition from a fossil fuel centred colossus of emissions to an “all of the above” source of diversified and, occasionally, low-cost energy. The phrase “just transition” will continue to annoy everyone remotely involved in the energy sector, much to the consternation and confusion of well-intentioned but clueless governments and the intellectual elite at think tanks, consultancies who advise them and the media. While billions continue to be spent on renewable capacity additions, the lack of attention to or love being shown to base load capacity continues to set the scene for recurring and rotating crises as the “grid” and the “consumer” struggle to balance affordability and availability. For industry participants, it’s precisely this type of chaotic destruction that creates opportunity. The smart players will straddle both worlds and become diversified “energy” companies and will secure the backing of capital providers who recognize the opportunity, aren’t intimidated by divestment movements or ESG box-tickers and will ultimately help manage the transition more effectively and efficiently than governments ever could.

This is a motherhood and apple pie prediction that can never be wrong. I’m allowed to give myself a freebie.

- Peak Oil Demand, much celebrated around the ESG world has now officially been pushed back, yet again, as demand for oil in 2023 is expected to exceed 102 mm bopd. Similarly, demand for natural gas will continue to grow to record levels. It is an accepted truth in the energy industry that demand for energy just continues to grow, even while the constituent components shift their relative share. Renewable growth, primarily in wind and solar, is getting more expensive so in order to meet immediate needs, fossil fuels are required to fill that gap. This means Oil. Gas. Coal. The business case on this is clear.

Yeah, this one was easy as well. Despite recession jitters, we just keep burning stuff.

- A prevailing theme across the energy sector (and the economy in general) is going to continue to be cost. Energy prices, while volatile, remain high. The costs for wind and solar are rising. Labour shortages are pushing up labour costs. And finally, the interest rate induced increases in the cost of capital is going to make every project that much more expensive, every hurdle rate harder to clear and every decision that much more difficult. I expect to see investment in wind and solar plateau and, conversely, investment in low hanging fruit fossil fuel projects, which are easier and typically cheaper to execute, to pick up. This is notwithstanding the governmental and regulatory headwinds that exist. All you need to do is look to Germany, where they permitted and built an LNG offtake facility in 5 months or where they have ripped down a windfarm to access coal deposits for how this can unfold. I’m not suggesting places like Canada could ever do the same, because well, business case, but they needed the LNG and someone is going to get it to them. Like Mexico, which signed a contract to ship LNG to Germany, gas that it doesn’t produce that is shipped to them on a pipeline built by a Canadian company. You can’t make this stuff up. At any rate, some of the energy decisions that make the least sense will start to unwind over the course of the year as governments seek to profit from their own sources and economically shelter their populations.

We will see about this one. The prediction that renewables investment may plateau while fossil fuel investment grows was pretty bold. Perhaps a better way to say it would have been relative growth rates might reverse. I’m not prepared to fully give up, but that statement was predicated on a recession. Apparently the only place where renewable investment is likely to slow is Alberta and that’s because the government chose to deliberately slow it down.

- Capex in the oil and gas sector is going to surprise to the upside in both Canada and the United States this year. How do I know this? I don’t. But it seems like the right call. In the United States, the Biden administration is going to want to add barrels back to the Strategic Petroleum Reserve and would prefer this to be done domestically – at worst using Canadian barrels. OPEC+++++++ seems determined to manage supply to prop up prices so the economics are compelling. It won’t be a runaway like the go-go light tight oil days, but 15% or more is on the table. Russian production is gradually ebbing as sanctions bite, but as mentioned above, demand is growing. Last year, every 1 barrel of decreased Russian production was met with 2.6 barrels of inventory and reserve drawdowns. This is unsustainable and investment in production needs to happen.

Clearly capex is a yearly measure but through Q3 we have seen accelerated spending in the United States and the winter and summer drilling season in Canada was the best in a while. Offshore is suddenly hip and cool again. Prices are in the right range, at least for oil. I’m all in on capex growth. Biden missed the window on refilling the SPR though. Q2 pricing saw some weakness and a bunch of rigs came on in the US, but with prices as high as they now are, refilling the SPR is a pipedream.

- The price of oil though 2023 is going to remain volatile. Absent any significant downward shock in the economy, change hostilities in Ukraine, an asteroid strike or some other randomly annoying black swan (see pandemic, land war in Europe), the price of oil feels trapped in a $70 to $90 range with A LOT of action in between. This is the glory call of the Forecast, which is of course why it is buried so low down. On top of the lack of investment in prior years, traditional suppliers will be unable to ramp up supply fast enough – Iran will likely still be under sanction and Venezuela has little to contribute, notwithstanding the recent rapprochement with Biden. OPEC isn’t meeting the quotas it cut, Mexico is pulling in its horns and Brazil is Brazil. This leaves the capital disciplined producers in Canada and the US to add any material incremental production into a pretty tight market. Moving capital from ESG index funds to some nasty Permian wells is going to be tough enough, wait until CNRL says they need some cash to do a brownfield expansion in the oil sands because TMX is almost ready. While this ironically (or fortuitously) leaves Canada as a place that can actually provide a steady, low decline and predictable supply, it will keep prices up. End of year price for oil is $84.59 (WTI) and the average for the year is going to be $81.37.

Well, it’s been quite the ride these past nine months. The price of oil has been under pressure for most of it, as recession fears, short sellers, a run-away US dollar and a lackluster series of domestic US consumption numbers overshadowed the realities of global growth in demand and the persistent lack of upstream investment, not mention OPEC+ doing its darndest to prop up prices but cutting back supply. Price at the end of Q3 was $90.79 and the average was $77.30. With the OPEC+++++cuts finally starting to bite and consumption a runaway freight train, I’m satisfied the direction is correct, but we still have a ways to go.

- Gas giveth, and gas taketh away. Last year was the greatest head fake a commodity as hated as natural gas has ever given. Prices rose through the winter to a producer’s sweet spot before shooting the moon after the Russian of Ukraine. Then a seemingly benign explosion at a US LNG producer started to let the air of the market and a warm winter in Europe sent prices scuttling for the exit. Where once we exalted prices per MCF in the range of $8, even $9, we now find ourselves lucky to approach $3 – in the middle of the hottest summer in memory no less! This despite record heat in the United States, low’ish storage, record consumption… record, record, record. Don’t even get me started on AECO. But really – what does any of this have to do with 2023? Well, lots apparently. The perfect storm for natural gas still exists. Russia is still not sending gas to Europe. A global market is forming. Consumption continues to rise. Canada still doesn’t have a business case for LNG. While US production sets records, it is still beholden to the big three shale regions (Permian, Marcellus and Haynesville) and any slip up could be cataclysmic. Accordingly, like in every year, I am bullish on gas. My year end call for natty is $4.89 per MCF and my average for the year is $4.37. At these levels, everyone makes money and Mike Rose and Tourmaline can continue to send me cushy dividend cheques. My downside risk to these prices would come if Canada evet got serious about a couple more projects and swamped the market… Ah, who am I kidding?

Who knew that the US would be able to produce so much gas? Not me apparently. Gas has continued to be a major disappointment as abundant supply swamped the market. Well, let’s be honest. It swamped the market where prices are set. California and New England gas prices are still bonkers, but in Louisiana where all the gas gathers? Well let’s just say they need more outlets. Maybe now that Freeport LNG is back up and running, we can see some positive movement. These low domestic prices though? Great for the LNG business case, know what I’m saying? Q3 ending price was $2.929 and the average was $2.54. Not exactly covering myself in glory here, but there are still three months left in the year for a major shortage to arise.

- The US closed out 2022 with 12 mm bopd of production. Some forecasts (ahem EIA) have floated that this could rise as much as 1 mm bpd by year end, but any simple math on initial production and decline rates will tell you that this would require completing up to 4000 wells which, simply isn’t going to happen. That said, it would be wrong to count out the Permian and GoM offshore production adds can move the needle. With my prior prediction of a 15% increase in domestic US Capex, it would be unfair to deny production growth. Assuming the price deck holds, capital costs don’t go too bananas and labour issues can be resolved, 5 mm bpd isn’t out of the question. However DUC counts are still lagging and the rig count has fallen throughout the quarter so there are challenges to production growth. In fact, the EIA even published a note saying production had fallen. Who knew THAT could happen!

Talk to me in 3 months, the current production level of 12.9 mm bpd is above the forecast but the monthly and weekly numbers are out of sync. All things being equal, I may have to take the loss on this one.

- In Canada, growth is expected to exceed that of the United States but not all of it is oil-directed. The pending completion of Canada’s two big pipeline projects in late 2023/early 2024 means that there are now shiny new tubes just waiting to be filled with sweet, sweet Canadian molecules. Whether it is an additional 537,000 barrels per day pouring into the Fraser River Delta (heh) or multiple BCF per day hissing towards Kitimat, the drilling prospects for Canada to fill these respective pipelines are bright. Here in Canada, we typically talk about drilling rather than production numbers and the real production growth is more likely a 2024 outcome, but it wouldn’t be unreasonable to expect a 5% increase in Canadian oil production over the course of the year and a similar increase in gas production. More important will be the 6,666 wells drilled over the course of the year, because that means jobs and prosperity for the service sector.

This is a year end number, but be prepared for me to completely miss the mark. Activity is robust!.

- Brazil gonna Brazil – overpromise and underdeliver.

Yup. Check this, while Petrobras continues to do its thing, Exxon has pulled out of Brazil.

- OPEC +++++++ production should remain fairly static unless prices start to move too far off the median sweet spot we seem to be in. Many nations claim to want to grow production but aside from Saudi Arabia and the UAE, none of the other OPEC members are very reliable at sustaining elevated production numbers for an extended period of time (Libya, Venezuela, Nigeria).

This is an odd one. Yes, OPEC is able to maintain its production at whatever levels it wants, be it high or low (unless we are talking about Nigeria and Venezuela). For Q1 they left well enough alone, but on April 1st dropped the production floor, then they got mad and formalized these cuts in quota and got really “discipliney” about it. Here we are at the end of Q3 and there is little sign of a break in the ranks. Don’t mess with OPEC.

- I am bullish energy stocks for the year. Consumption isn’t slowing and the price deck is favourable. Cash flow and dividends will continue to accrue to shareholders as will buy-backs. And now that debt has been paid off, look to some reinvestment into production. My genius stock picks that will power your portfolio will follow in a bit, but I would look to cash flow juggernauts like Canadian oilsands producers, gassier names with exposure to LNG Canada and, I know I’m going to regret this, a quality upstream service company.

I’m still all-in here. Mainly because as someone with a full-time “job” I don’t get the luxury of trading energy stocks so I have a lot of buy and hold nonsense happening. That said, with the mid summer price swoon finally out of the way, everyone is once again (still?) making money hand over fist. Dividends are flowing, debt is a thing of the past and even the Canadian gas names just shrug off $. Like seriously, they have dealt with AECO long enough to know…

- The M&A market should be strong this year except for that one nasty variable. Cost of capital. No acquirer in their right mind is going to make an aggressive move unless they have some line of sight as to when the current tightening cycle will, if not end, then at least temper itself. This suggests that any significant M&A will be a second half story, at least on the producer side. In the service sector, with the anticipated growth in drilling and industry-wide manpower and supply chain issues, there will be deals done throughout the year as companies attempt to secure their client base and steal market share from less well-capitalized competitors. This will be less apparent to observers because this service industry activity will occur amongst the mid-market private companies (yay for our business!) but it will be there and, I believe fairly well distributed from upstream to downstream. Those companies exposed to the big projects like TMX and CGL will be less of interest as those projects wind down, but with TMX especially, the market for acquiring that asset will heat up, more likely in 2024. Thinking more broadly, with the US Dollar wrecking ball in full swing, it can be safely said that relative to the United States, Canada is “ON SALE” and American buyers should be paying attention to the Dollar Store to the North.

Apparently the producers have decided that cost of capital uncertainty isn’t all that big an obstacle as I thought and the M&A world has been way more active than I anticipated in the first half of the year, especially in the US. Baytex announced the acquisition of Ranger Resources in the US in February to get the ball really rolling and others joined the party – like Crescent Point buying Spartan Delta assets at the end of March. Q2 promises even more fun, with the ever-puzzling Ovintiv out-Newfielding itself by buying $4.7 billion worth of tight oil assets from EnCap. It’s on baby! Then of course there is Conoco buying Total Energie’s interest in Fort Hills Surmont. PDC was acquired by Chevron for $6.3 billion. Civitas bought a small Permian Basin asset package from NGP Partners for $5 billion. Ranger Oil was bought by Baytex for $2.5 billion (yay Canada!). Civitas also bought Hibernia Resources from NGP (hmm). And that was just June! Then there were a bunch of midstream deals announced worth mega-billions. And Warren Buffett continues to add to his position in Oxy. For a sector that is an economic pariah, there sure seems to be a lot of interest. Must have something to do with solar panels. Even the publicly traded Canadian service sector is trying to get in on the action with CWC Energy Services selling to Precision Drilling!

- Still waiting on a prominent Canadian name to take itself private. Last year I thought it would be Whitecap or Baytex. It didn’t happen. But it makes sense. Someone needs to take the plunge – Baytex? Come on guys…

OK, I guess Baytex is out, but I’ve noticed that Mike Rose has been accumulating an awful ot of shares lately.

- And my evergreen M&A statement on Canada: Canadian companies are well-known for their technology and solutions-based approaches to innovation and there is a well-worn path of US PE and strategics coming north of the border to snap up cheaper Canadian tech. With an uncertain market in the United States, look for these companies to draw interest, particularly ones that have technologies that address emissions or can reduce costs in an inflationary, supply-chain challenged world. Also, Canada is a currency advantaged, undervalued and stable market for consolidators tired of the madness in other markets. Global recovery and growth indicates a commodity super cycle, likely the last big run of my career. Show me the money people!

It’s an evergreen statement for a reason. We are seeing A LOT of interest from American buyers.

- The Canadian dollar should be performing way better than it is with commodity prices at their current level. As a Greek hotel manager in Athens said to me once when I staggered in with heat stroke from 38 degree temperatures: “Why are you so weak?” Well, I will tell you why. A weaker less resilient economy beholden to non-productive asset values. A government perceived as hostile to big ticket industrial investment (it doesn’t have to be true to affect things). Terrible relative productivity numbers that keep getting worse. A bank rate a few basis points light relative to the Fed. Put another way, why buy Canada? The Canadian dollar is lucky to be at $0.76. It will be lucky to be there at the end of the year. I give it $0.743.

In more of an “isn’t this annoying?” vein, the Canadian dollar managed to languish around the $0.72 mark for much of Q1 and chunk of Q2 coinciding of course with my own personal travels to the US, where everything is not only priced in US dollars so 35% higher to us Canucks, but often 10% higher anyway. Someone should really pay attention to this disparity. I kinda think it matters. Anyway, thanks to OPEC and their production cuts, we ran back to $0.75-$0.76 but don’t count on it becoming a runaway since I have travel plans to the US. True to form – October Canadian Peso was at $0.73. I blame Trudeau.

- Inflation will continue to cool off over the course of the year. But don’t let the politicians and pundits fool you. The damage is done. Energy costs may come off but without significant deflation across the board, everything has gotten 10% to 15% more expensive and that new price level is here to stay. We may get some relief when house prices come off a further 10% but we will need to wait to see that trickle through the numbers. I fully expect inflation in Canada and the US to be within the policy ranges by the end of 2023, hope you enjoy your $9.99 eggs and $30 caesar salad..

Eggflation seems to have crested and a gradual reduction in inflation is happening. Wit the recent runup in oil and gas prices, I may be optimistic at how fast – end of 2023 may very well be Q1 24. Note that the latest CPI reading in Canada was close to the policy range of 1%-3% but… and it’s a big but – food continues to rage out of control as does accommodation costs (this is what happens when you raise rates) and the forementioned energy prices.

- Interest rate increases as well have run their course. Central banks will be elated at all the policy room they have to combat the recession they caused. Holders of variable rate debt will just have to take that up with their banks or the guy with the crowbar who gets the outsourced collection work. All kidding aside, the economy feels like it is slowing a lot faster than the trailing numbers suggest. So 5.0% is the new 2% which a while back was the new 0.25%. No matter what this is here for a while and we are unlikely to see any easing of consequence in 2023.

Yup. We are all bored of these interest rate increases and the havoc they are causing to the banking sector and personal finances. All of us except Jerome Powell who of course who hates everyone and everything. I think Canada is all done with the rate increases (is anyone paying attention?) and the Fed maybe has another 25 basis points to go, just because, but I think this is a win. US rates are at 5.25% and I think psychologically, JP is planning to overshoot just to wreck the stock market. Maybe we end the year at 4.75% when the A bots realize that the tech rally was a huge lie and sell their last positions of overvalued and overhyped glorified chip manufacturers – the great rotation from Nvidia to Frito-Lay can’t come soon enough. Welcome to the future.

- The effect of interest rate increases still needs to work itself out in asset values as well as corporate valuations. An implicit component of corporate valuation is a Weighted Average Cost of Capital that is applied to future earnings. Currently the interest component of that WACC has more than doubled and the prospects for future earnings has been revised, downwards in case you were wondering. This should translate into a further deterioration of value in both publicly traded and private companies in growth oriented or interest rate sensitive industries. Translation – tech and real estate still have room to correct.

I’m still waiting for this. The math is there for all to see. But the market apparently doesn’t respect math. Someone, somewhere is going to get burned. Logic says it has to be tech investors. Recent history says it’ll be oil and gas stocks, just because. The housing market correction is playing out in weird ways, largely due to scarcity, but a 10-15% correction is needed. Sorry everyone.

- The TransMountain Expansion and Coastal Gas Link will both be, for all intents and purposes complete this year which will count as something of a Canadian miracle (or in French, un miracle). The NGTL project recently approved by the Canadian government will get underway in earnest over the next year with the goal of fixing AECO and other Canadian gas pricing. But aside from that, there are no significant pipeline projects on the horizon. I don’t know whether it has to do with a lack of a business case or fear of government, I suspect a combination. It would be nice to see a new LNG mega project get a start, especially now that the pipeline infrastructure has caught up, but I don’t hold out much hope. Here in Alberta, hopes are being pinned on some Carbon Capture projects getting a kick start, but I wouldn’t hold my breath. On the renewables side, Alberta will continue to be the national green pariah while also continuing to lead the country in actual wind and solar infrastructure investment. It’s fun to live in a place so full of contradictions.

Well would you look at that. Cedar LNG, an indigenous led LNG project in BC managed to have enough a business case to get approval from both the BC and Federal governments. I guess the Impact Assessment Act really works. Sort of. The rest of my project narrative holds true.Didn’t count on Alberta putting a pause on renewables approvals but we are a weird province. Middle East unrest may prompt the US to blow the dust off the KXL file – I give it a 0.5% chance.

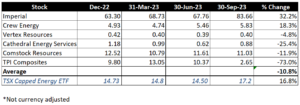

- My two favourite Canadian E&P picks for the year represent what I said earlier. Oilsands exposure and BC focused natty player. With just that as a guide, we all know you can’t go wrong with either of Imperial Oil (time to go with a classic!) or Crew Energy, because who doesn’t like a company with Montney gas and Lloyd heavy oil exposure? Sure, I could have gone with CNRL and Tourmaline, but I wanted to be edgy.

OK, well then. A few minor issues with Imperial – something about seepage and leaking taiings ponds – nothing to see here. Crew pretty much under the radar. Ironically, Imperial is my best performer – Let’s Go Leaks!

- On the service side, I’m going to go with my gut and pick wafer thin trading microcap Vertex Resources because I like the team, the strategy and where they are going and then I will move upstream and ride Cathedral Energy Services to upstream drilling glory.

No one did well in the first or second or third quarter for that matter despite high activity levels, maybe these micros are an end of year play? Maybe I need stocks with liquidity? I remain hopeful but the trend is not my friend.

- In the United States I typically pick a producer and some weird flyer that no one has ever heard of that destroys my credibility. True to form, I will follow that policy. Pick number one is Comstock Resources, otherwise known as the Peyto of the US (actually, I made that up) – a pure play natural gas producer and Vision Energy who represents my current year venture into renewables development and implementation as opposed to subsidized solar installation which crushed me last year.

A pure play natural gas producer seems counter-intuitive, but it’s actually just a bad pick. Let’s see how the end of the year plays out. As noted earlier, I dumped Vision (which was a scam) for TPI Composites – they make blades for wind turbines. Manufacturing is where it’s at, right? Not some fly by night fake company? Neither is heading in the right direction. Sure, TPI had a positive return, but that was Q1 and apparently blades for turbines are worth bupkus.

- Bonus forecast – Twitter will survive. Elon as well. Recent changes are annoying but it’s only as toxic as you let it be.

Jury is out. But it sure is toxic. And now it’s called X. So I guess it didn’t survive after all. Still no blue check for this bad boy.

- Bonus stock pick? Anything Cannabis related. I have a feeling that with inflation, interest rates, recession, falling house values and political chaos the use of maryjane is going to skyrocket.

Well, I found a cannabis ETF and it’s down 43% so far this year. Jury is out!

- Sports? Sure. Super Bowl – Buffalo beats Minnesota. Stanley Cup – Boston beats Calgary. NBA – don’t care.

These are bonafide fails. Especially the Super Bowl pick. Boston was a great pick for the Stanley Cup except they were whipped by a former Flame. NBA? Never mind..

That’s it!

My grade so far is like 16.5 out of 30 or 56.7%.

It’s going to be a long and wild three months.

My time here is done.

Invest wisely.